Before tackling your 1031 exchange, take a few minutes to consider the most important 1031 exchange rules. Among these, the exchange deadlines imposed by the IRS are one of the easiest rules run afoul of. In fact, there are very few rules that the IRS takes more seriously than the 1031 exchange deadlines.

Below, you’ll quickly learn about the 1031 identification period and why it matters so much, plus how long you have to complete an exchange.

Let’s get started.

Under the Treasury Regulations, any 1031 exchangor must formally identify any potential properties that you are considering purchasing to complete your 1031. Moreover, you must do this within 45 calendar days (a month and a half) of closing on your relinquished property. This is nonnegotiable.

“Identification” seems like a vague term, but there are important requirements and guidelines to follow. Your 1031 identification must:

During your 45 day period, you can modify, remove, or add to your identified properties list as often as desired. If you find a more impressive asset on day 22, you have every right to identify it. Come day 46 after closing, however, you’re locked in. No more changes. And you can only successfully complete your 1031 exchange by closing on at least one of the properties you identified in the first 45 days.

The 1031 identification period should not be taken lightly. If you don’t identify any properties within the 45 days, you’ll have no assets eligible for an exchange, and you’ll owe capital gains tax on the property you sold.

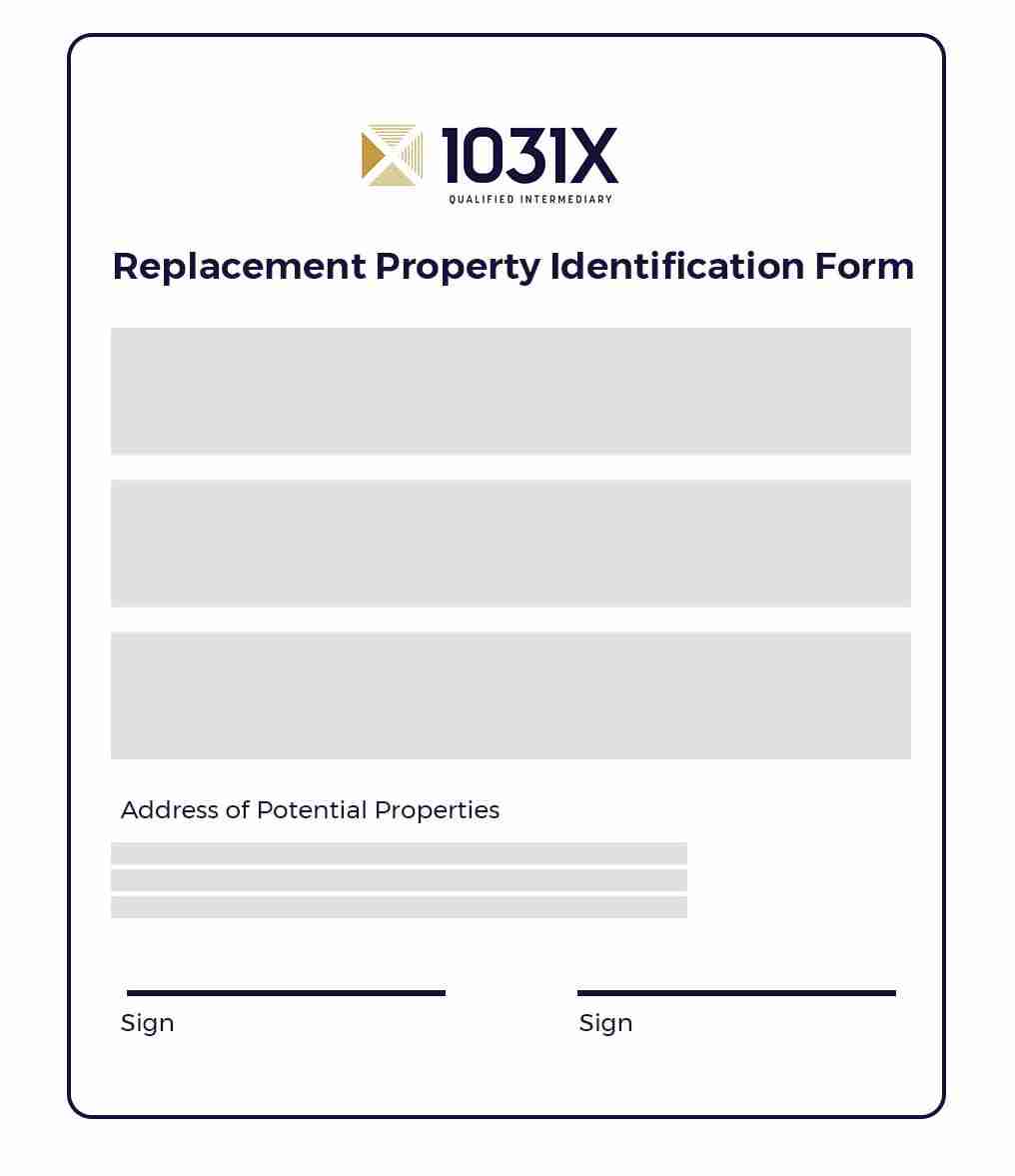

To make this easier, we have our clients use an interactive online ID form:

Replacement Property Identification Form

We’ll explore this form a little further soon.

That’s because you need to know the 3 – Property Rule.

(Note: A signed contract, letter of intent, or other negotiated agreement can count as your identification so long as the property is unambiguously described therein)

Replacement Property Identification Form

We’ll explore this form a little further soon.

That’s because you need to know the 3 – Property Rule.

(Note: A signed contract, letter of intent, or other negotiated agreement can count as your identification so long as the property is unambiguously described therein)

Important note 1: The properties you identify do not have to be under contract. You do not have to have made an offer, and you are not required to make an offer. The properties identified do not even have to be listed for sale.

Important note 2: For counting purposes, the day that you close on your sale is considered Day 0. The following day is Day 1. All holidays and weekends count.

The IRS limits you to only identifying up to three properties at any one time during the identification window. Your identified properties do not lock you into an exchange with all of them, but they will be the only properties eligible.

Remember, your list can be changed during the 45 days, but the three property limit stays in place the entire time.

Here is an example:

As long as you identify three or fewer, you can list properties of any value.

Is the 3-property rule absolute? No. But almost all 1031 exchangers stick to just three properties. And the reason is that, when you identify three or fewer properties, there are also no value restrictions to what you can identify.

As you’ll see next, this changes as soon as you identify four or more properties.

The IRS allows you to identify more than three properties, but there are added conditions. Specifically, you must now follow either the 200% rule or the 95% rule.

The 200% rule states that your 1031 exchange is only valid if the collective market value of your 4+ identified properties is less than 200% of the net sales price of your relinquished property.

Here is an example:

Remember, to defer all taxes in a 1031 exchange you must acquire replacement property(ies) worth at least as much as your net sales price. By identifying many smaller-value properties, Jane Doe must now successfully compete for and close on several properties to receive full tax efficiency.

There is one additional way around the 3-property rule and the 200% rule.

In a 1031 exchange, the 95% rule —which is very uncommon — allows you to identify 4+ properties of any market value. However, to qualify under this rule, you must successfully close on 95% of the total identified market value on your 45-day list. For instance, you might identify seven properties with a combined value of $3,000,000. In this case, you can only complete an exchange if you purchase at least 95% of that value — or $2,850,000. This effectively means that you must purchase every single asset on your ID list within your exchange window.

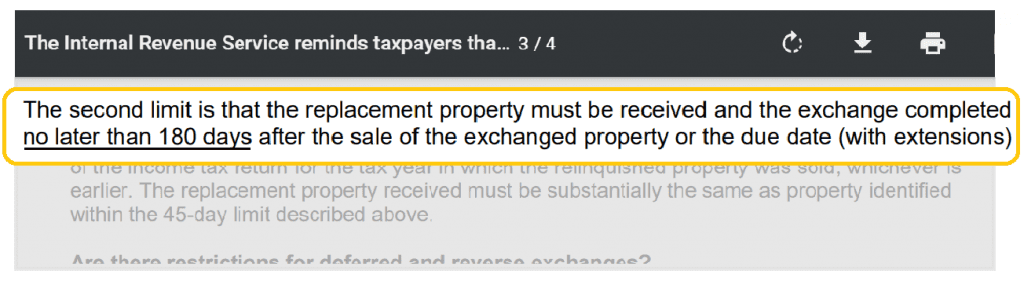

The second deadline in the 1031 exchange timing rules is the “180-day” window. From the date you sell your relinquished property, you have 180 calendar days to complete your exchange (or 135 days following identification).

A complete exchange means:

If you purchase multiple properties in your exchange, you must close on all of them within the 180 days. Selling your relinquished property always triggers the countdown. Our advice? Stay as organized as you can (which we help with).

Important note 1: It is OK to close on a replacement property prior to the end of your 45-day ID window. This property will count towards your 3-property limit.

Important note 2: Your sale closing is considered Day 0 for counting purposes. The following day is Day 1. All holidays and weekends count.

At 1031X, we make exchange deadlines simple. Our online client portal makes property identification incredibly fast and easy. Fill out the information for your three properties, sign it, and you’re good to go.

We have automated procedures and hundreds of years of combined experience performing 1031 exchanges in all 50 states (plus D.C. and territories). Plus, you work with a personal consultant throughout your exchange. Call, email, or chat with them through the online portal and get every question answered.

Whether you are brand new, or need an advanced strategy, this is your go-to center for Section 1031 Exchanges.

Exchange expertise, built over 32 years.

1031X is a nationwide Qualified Intermediary specializing in 1031 exchanges for residential, commercial, and multifamily investment real estate. We facilitate forward, reverse, construction, and complex exchanges under IRS Section 1031 — with documented governance, insured escrow protection, and structured execution since 1994.

1031X.com, Inc. is a Qualified Intermediary as defined under Treasury Regulation §1.1031(k)-1(g)(4). 1031X does not provide legal, tax, or investment advice. Some licensed professionals may participate in 1031X’s partner network and may receive marketing or referral consideration, educational sponsorship, or charitable recognition consistent with IRS, state, and federal disclosure requirements. 1031X maintains independence and does not share revenue from settlement or investment services covered by RESPA, SEC, or FINRA regulations.