Advanced Strategies

Major Topics

When to Use Advanced 1031 Strategies

This page offers a modern breakdown of advanced strategies and tactics for 1031 exchanges.

It’s for those times when a standard 1031 won’t cut it.

And you need to get creative.

Now, some of these may increase your tax risk. Thankfully, 1031x has been at this for decades. We’ll show you how to use these safely

So when should you consider one?

Let’s review.

Reverse

When you need to buy the replacement property before you sell the relinquished property.

Construction

When you want to make improvements — or build something brand new — using 1031 proceeds.

Primary Conversion

When you want to 1031 exchange into or out of a personal residence, whether primary or vacation.

Refinance

When you would like to pull out equity from exchange property rather than reinvesting 100%.

Related Party

When you want to buy property from a family member to complete your 1031 exchange.

Owner Carryback

When you want to finance the sale of your relinquished property through an owner-carry loan.

Reverse

When you need to buy the replacement property before you sell the relinquished property.

Construction

When you want to make improvements — or build something brand new — using 1031 proceeds.

Refinance

When you would like to pull out equity from exchange property rather than reinvesting 100%.

Primary Conversion

When you want to 1031 exchange into or out of a personal residence, whether primary or vacation.

Related Party

When you want to buy property from a family member to complete your 1031 exchange.

Owner Carryback

When you want to finance the sale of your relinquished property through an owner-carry loan.

Reverse 1031 Exchange

A reverse exchange allows you to capture the replacement property before finalizing your 1031 sale.

Plenty of clients do this when

- Their sale becomes delayed (or falls through)

- They want to quickly claim a property in a hot market

- They know what they want to buy, not what they’ll sell

But it’s not easy. There are many hurdles.

We’ll show you how to avoid them.

Don’t Simply “Buy First, Sell Second”

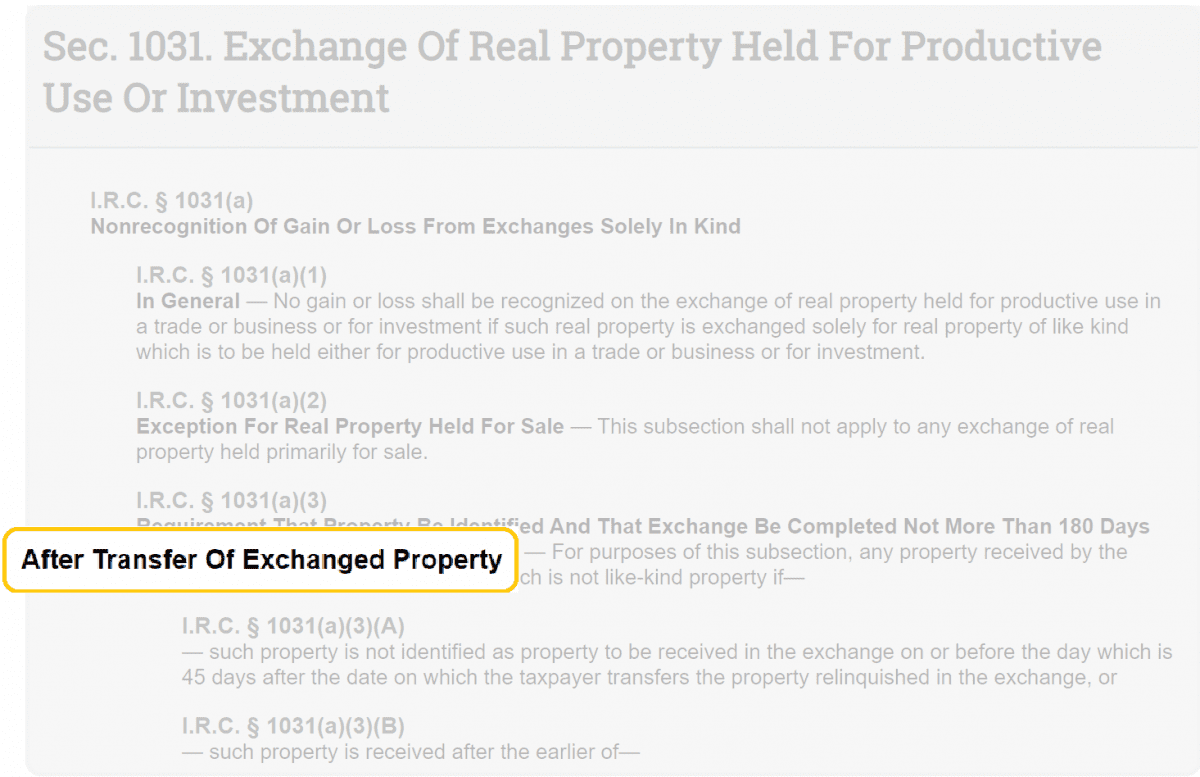

The regulations do not authorize a “buy first, sell second” like-kind exchange.

This is implicit in I.R.C. §1031(a)(3), which says that tax deferral is possible only after transfer of exchanged property.

In other words:

If you want to buy before you sell, you have to get creative.

The trouble is, certain brands of creativity get labeled as “tax evasion”.

Not good.

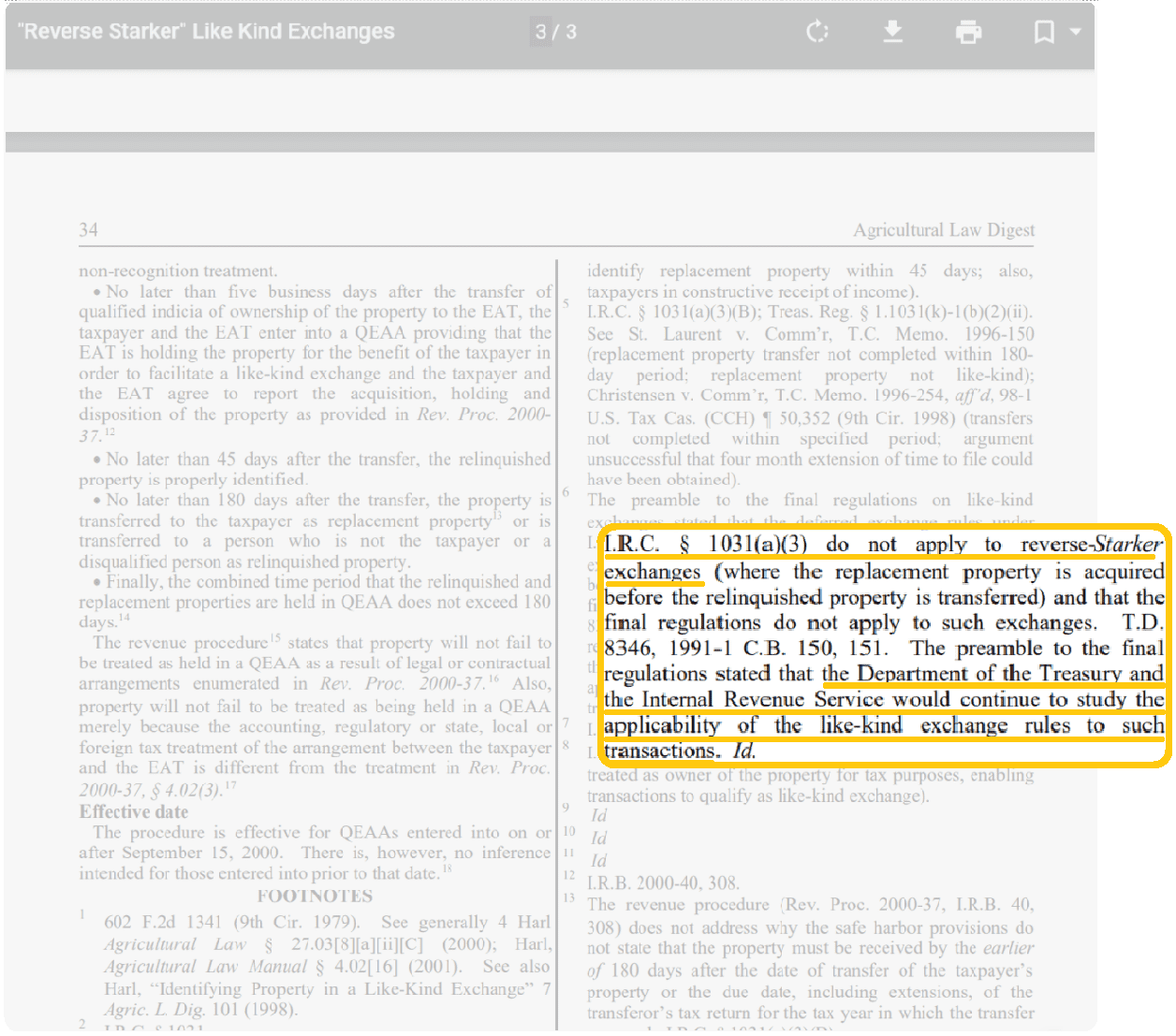

After the initial 1031 laws were written, the IRS promised to study whether to allow “reverse-Starker” exchanges.

(Starker was the 1920s legal case that created 1031 exchanges)

The IRS ignored this promise for decades.

Finally, an acceptable process for “reverse” 1031 exchanges arrived with IRS Revenue Procedure 2000-37.

This new ruling legitimized some very useful techniques.

Specifically, now you can make a reverse exchange look like a “sell first, buy second” exchange.

Just like any other legal 1031.

Let’s discuss how you do it.

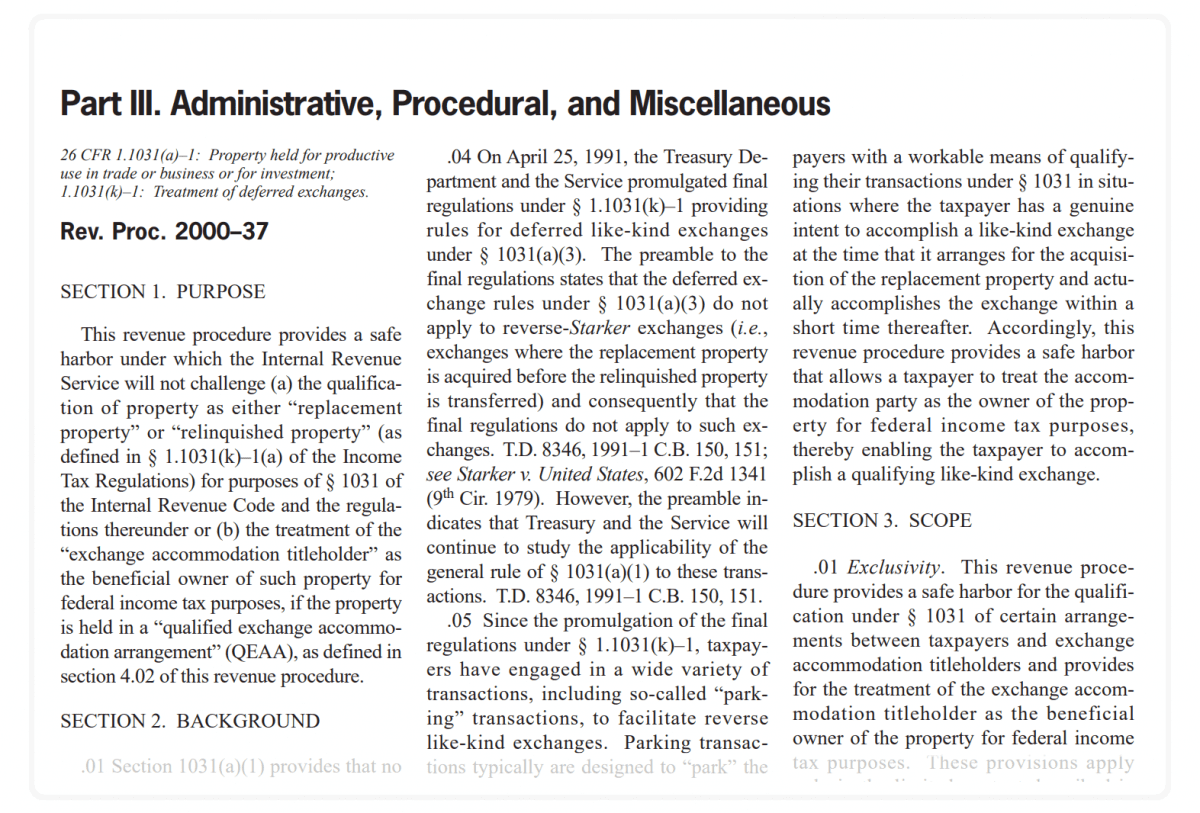

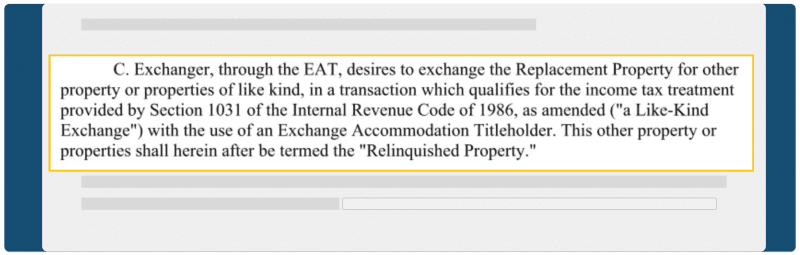

Set Up an Exchange Accommodation Titleholder

Here’s one of the weird parts:

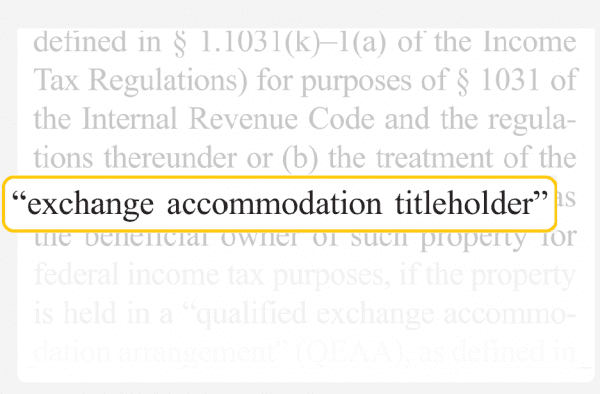

Under IRS guidelines, investors may “park” their relinquished or replacement property with a third-party holding company.

The IRS calls this an Exchange Accommodation Titleholder (“EAT”)

Creating an EAT is a very important part of the reverse exchange process.

Today, most EATs are set up by your Qualified Intermediary.

How does the EAT “park” a property?

There are two basic reverse exchange parking strategies:

Strategy #1 – The EAT buys and holds your replacement property.

- After you sell your relinquished, you buy from the EAT.

- Also called an “Exchange Later” reverse 1031.

Strategy #2 – The EAT buys your relinquished property.

- Next, you buy your replacement.

- Later, you find a permanent buyer to purchase from the EAT.

- Also called an “Exchange First” reverse 1031.

In either case, you (the taxpayer) can now demonstrate that followed the correct order — sale, then purchase.

Pro Tip: Having the EAT purchase the replacement property is often the easier solution.

Sign a “Qualified Exchange Accommodation Arrangement“

Here’s some good news.

The IRS has very specific rules about structuring a reverse 1031 exchange.

Why is that good news?

It gets rid of ambiguity. Your exchange is more likely to succeed if you follow their roadmap.

In fact, Rev. Proc. 2000-37 says that the IRS will not challenge the inclusion of a property in a reverse exchange — or its being held by an Exchange Accommodation Titleholder — so long as you have the correct legal arrangement.

That means signing a Qualified Exchange Accommodation Arrangement (or “QEAA”).

Qualified Exchange Arrangement

Not surprisingly, nearly all 1031 companies use this same legal form for reverses.

Stick with what works.

That’s what we do.

What does the QEAA do?

The QEAA is mostly useful because it tells the IRS that you intend to follow its rules.

Our agreement says the following.

In a nutshell, it says “I’ve read Rev. Proc. 2000-37 and my exchange will comply accordingly.”

Here’s more:

- It states the EAT will hold the “parked” property for benefit of the taxpayer in a 1031 exchange.

- The EAT accepts responsibility of owning real estate for all federal income tax (and tax reporting) purposes..

- The taxpayer agrees to follow 45-day and 180-day deadline rules upon purchase of the parked property by the EAT.

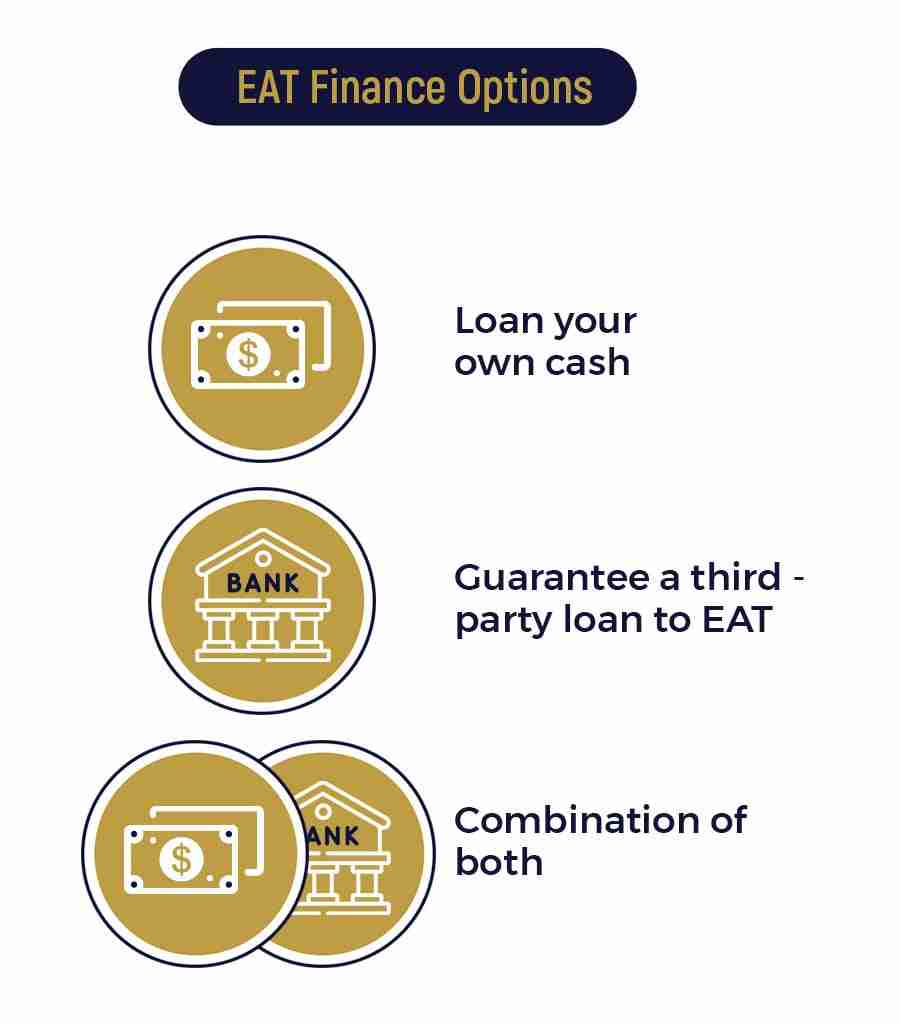

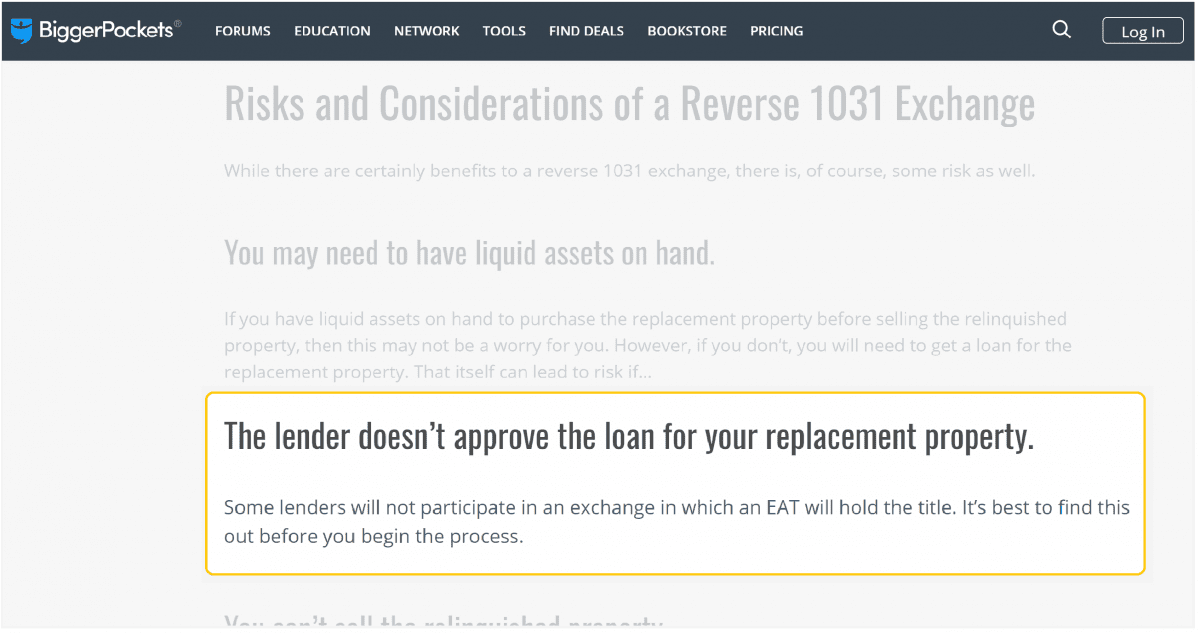

Secure Financing for the EAT

This is something a lot of reverse exchangers struggle with.

The EAT has no money.

As such, the EAT must borrow 100% of the funds necessary to purchase the parked property.

And it’s your job to figure out how.

Investors that succeed with reverse exchanges do one of three things:

Option #1 – Loan your own funds to EAT

This is the easier option BY FAR.

After all, traditional lenders don’t like “parking” arrangements.

If you have the liquidity, you should consider using it. Especially if you were prepared to pay cash for the replacement property anyway.

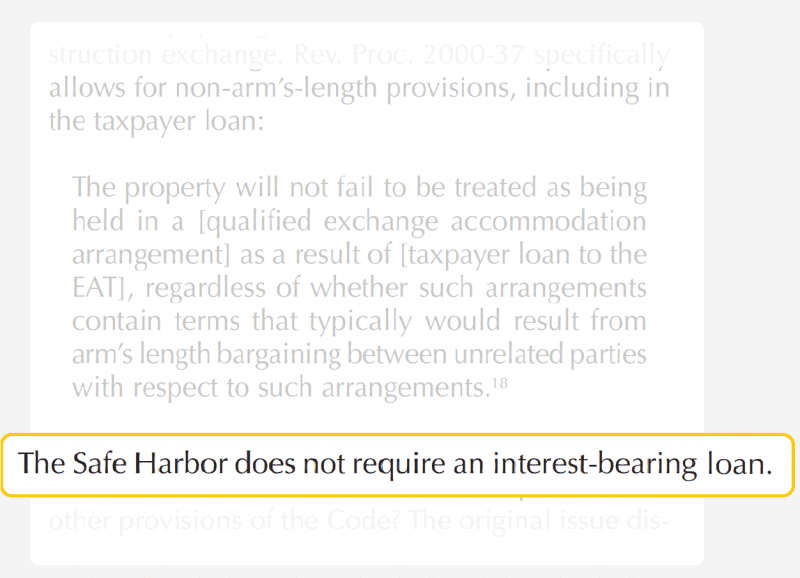

What about loan terms?

If you loan money to the EAT directly, that loan does not need to bear interest.

(Source)

Option #2 – Guarantee loan to EAT by third-party

Most mortgage lenders and banks don’t want to loan money to any LLC. This is doubly true for an EAT.

The issue is that the EAT doesn’t have any assets or borrowing history. Very few lenders understand the whole strategy.

Which is why many exchangers personally guarantee any loan made by a third-party.

In some cases, the exchanger offers up extra collateral.

Option #3 – Combine loans

If the third-party lender isn’t willing to lend 100% of the necessary funds, then you have to make up the difference with a cash loan to the EAT.

Close on Property Through EAT

Funding is the difficult part. After that, closing is pretty easy.

→ EAT is buyer/borrower

→ You (or third-party) act as lender

→ Qualified Intermediary makes sure the rules are followed

Again, the EAT can purchase either the relinquished property or the replacement property.

Relinquished property

Have your attorney or QI draw up a purchase and sale agreement. You are the seller. The EAT is the buyer.

Replacement property

You should already be under contract to purchase the replacement.

Now you have to assign your rights as buyer to the EAT. For some contracts, this may require amending the contract to allow for assignment.

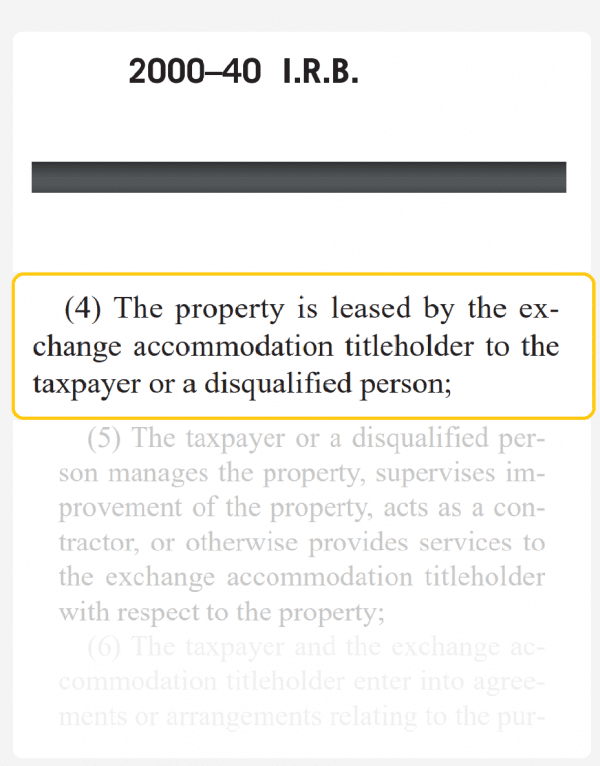

Lease Property from EAT

No matter which property you parked, you still want control over it.

So you need a lease.

This secures access to the property even though your exchange is still ongoing. The IRS has no issue with this structure.

In effect, the EAT becomes your landlord.

(Use a NNN lease to maximize your control)

What About Rental Payments?

This is a little complicated.

For starters, most experts agree that any lease from the EAT to the taxpayer does not need to charge a rental payment.

That said, some still do.

And here’s why:

Let’s say the EAT borrows money from the taxpayer or a third-party to buy the replacement property. And this loan carries interest.

Well, the EAT may need to make mortgage payments AND declare an interest expense on a future tax return.

By charging the right amount of rent, the EAT can balance out the mortgage payment and also offset the interest expense.

Key Takeaway

Talk to your QI about whether your lease needs a rental payment.

Complete “Forward” Part of Exchange

OK, the tough part is over.

Now it’s time to complete the “forward” part of your exchange.

The are two different ways to complete the reverse 1031.

Let’s break them down.

#1 – EAT “parked” the replacement property

- 45 calendar days to identify up to three potential relinquished properties.

. - 180 calendar days to sell relinquished property and then take title to the replacement property..

(These are just the inverse of normal 1031 exchange clocks)

Your relinquished property closing will look like any other “forward” 1031 exchange.

- You need a QI

- QI sets up an escrow account

- Proceeds from sale go directly to escrow account

As soon as you are no longer on title to the relinquished property, then you can go ahead and complete the 1031 exchange by taking the “parked” replacement property.

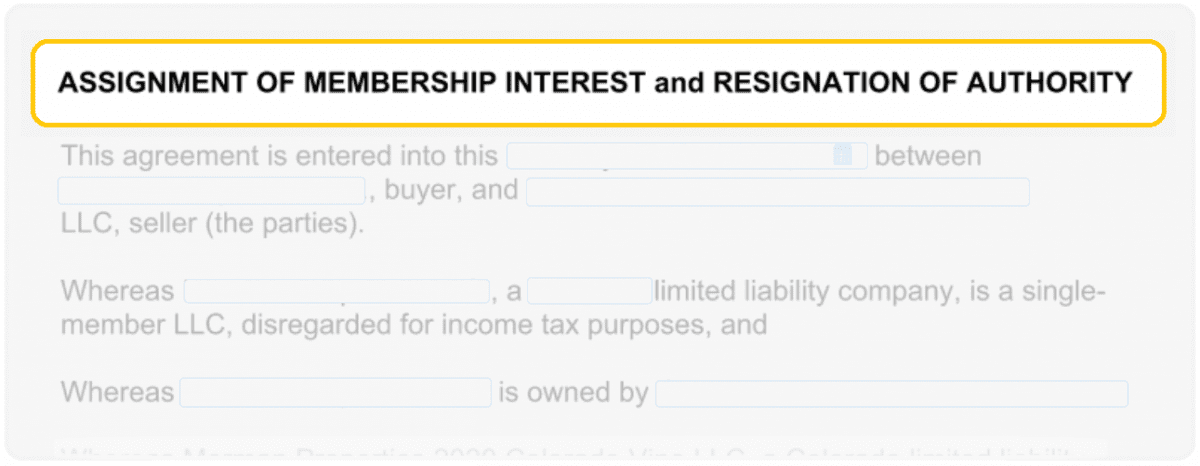

There are two more methods for taking the parked property.

- Your QI will assign to you the membership interest (i.e. ownership) of the EAT.

- Execute an “Assignment of Membership Interest”

- As consideration, the proceeds from your sale will be used to repay the original loans to the EAT

.

- You will re-deed the property. This means the EAT will sell to you directly.

- Formal closing

- QI or attorney should draft contract

- Proceeds used to repay loans to EAT

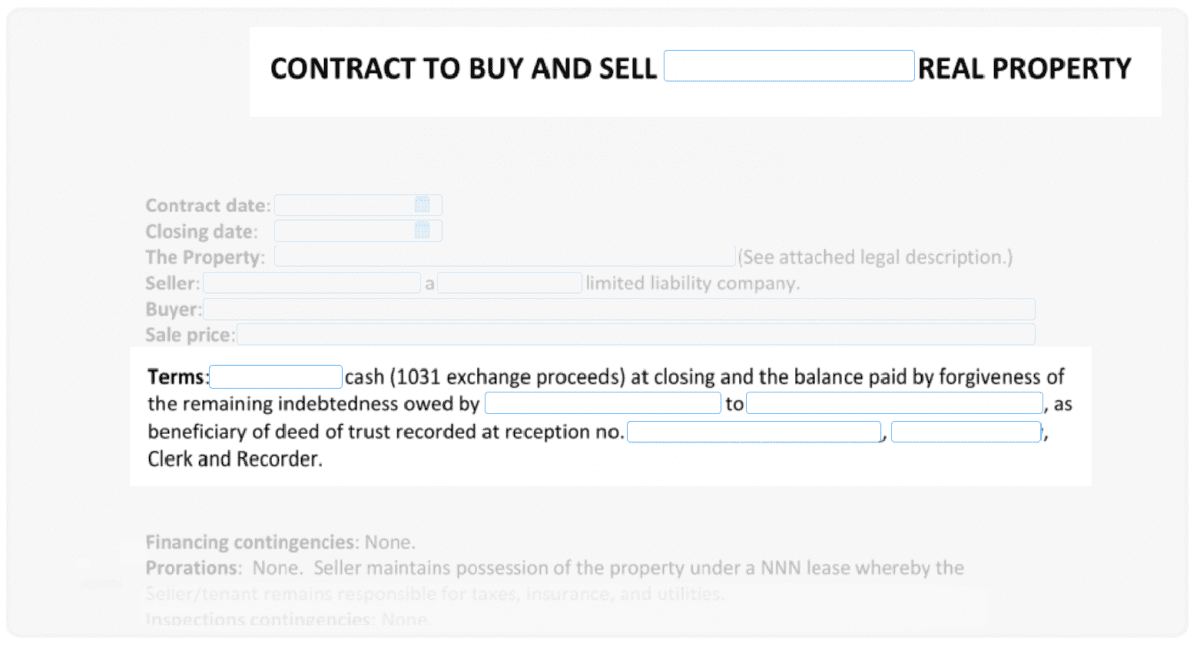

#2 – EAT “parked” the relinquished property

This one’s trickier.

Parking the relinquished property isn’t as natural as parking the replacement.

But there are reasons to go this way. For example, some lenders refuse to work with EATs.

Here’s a common model:

- lender won’t allow EAT for replacement

- QI drafts a simple contract for relinquished

- EAT borrows money from the taxpayer (i.e. you)

- could be cash loan

- could be assumption of remaining debt

- could be seller carryback loan

- probably will be a combination of the above

- EAT closes and takes title

- property leased back to taxpayer

- taxpayer keeps looking for permanent buyer for relinquished property

The EAT isn’t going to market your property.

You will. (And your broker)

And you negotiate everything — price, timing, contingencies, etc.

Try to settle on the same price that the EAT paid. If the property sells for less than what the EAT “paid”, the EAT does not owe you the difference. If it sells for more, the EAT may pay you the excess.

The second half of your exchange continues per normal.

You buy the replacement property using escrowed funds (if any) from the sale of the relinquished property to the EAT.

Important Note

The relinquished property should not sit with the EAT for more than 180 calendar days.

Construction 1031 Exchange

A construction exchange allows you repair, improve, or build new structures within a 1031.

We see clients do this when

- Their replacement property isn’t quite valuable enough

- They can’t find a replacement they like (and so would rather build one)

- Their replacement property needs some TLC

The IRS doesn’t like these very much.

But they still allow it under the right conditions.

Let’s explore.

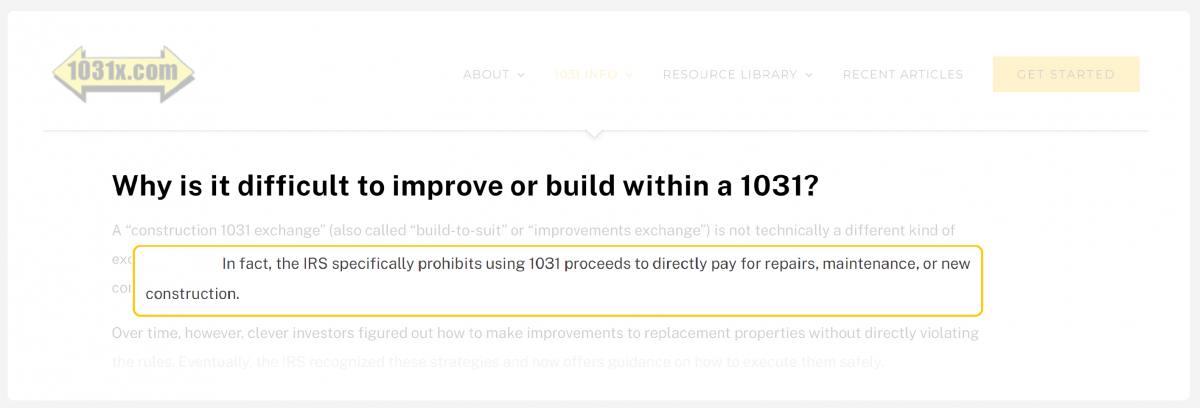

Don’t Directly Use 1031 Proceeds to Fund Improvements

Here’s the most basic rule:

Don’t directly use your sale proceeds to pay for improvements.

Why not?

There are specific prohibitions against doing so.

The IRS classifies improvement purchases as either labor or materials.

Not “like-kind” to real property in a 1031 context.

So you need a creative workaround.

(More on that soon)

Don’t Improve Property You Already Own

OK, here’s a second rule.

You can’t improve or develop property you already own.

Now, in all fairness, this is actually a VERY complicated topic.

But for now, just remember that any improvements should be made before you take title to a replacement property.

How?

Set up an Exchange Accommodation Titleholder.

This new entity will purchase and hold the replacement property for you.

Then, while the Titleholder owns the property, you direct the improvements that you want.

Let’s discuss that next.

Assign the Replacement Property Contract to an EAT

So you need an Exchange Accommodation Titleholder (EAT) to pull off a construction exchange.

We covered EATs in detail in the Reverse section.

So we don’t want to repeat everything here.

Short story:

- The EAT is a new limited liability company (set up by your Qualified Intermediary)

- You are not a member of the EAT

- The EAT borrows 100% of purchase and improvement funds

- The EAT purchases and takes title, not you.

But the EAT isn’t going to negotiate with the seller for you. You have to sign a contract with the seller, then assign your rights under that contract to the EAT.

The terms of the contract will not change. The EAT will buy at the same price, on the same date, and with the same contingencies in place.

You need to arrange financing for the EAT.

This can get complicated, as we explored in the Reverse strategy above.

If you manage to pull this off, the next part is to start improving the replacement property.

Let’s see how.

Sign a Project Management Agreement

Even though the EAT buys the property, you want to oversee the improvements directly.

(After all, this is going to be your property at the end of the 1031)

So your intermediary will have you sign a Project Management Agreement. This gives you several powers and responsibilities:

- Make improvements (or contract to do so)

- Perform the requirements for any contracts

- Seek and comply with permits

- Consult and retain third-parties

(such as legal counsel, engineers, contractors, etc.)

Oversee the Improvements

You, the taxpayer, handle the improvements

To be clear:

We are not experts in making improvements.

That’s up to you.

Intermediary handles the 1031 rules

But we can help you with the planning.

The entire 1031 process — EAT purchase to improvements to completing the exchange — should take no more than 180 calendar days.

So you want to be REALLY organized.

For example, we see clients get stuck behind permitting and zoning bureaucracies. Others may not have the full scope of their improvements hired out.

It’s important that you communicate your deadlines with contractors.

All payments to your contractors should flow through the EAT.

You need to work with your 1031 coordinator to make sure payments can be made accurately and on time.

Transfer Improved Property (or the EAT) to You

Just like an “Exchange Later” reverse 1031, there are two options for unwinding a construction exchange.

Option #1:

Draw up a simple purchase and sale agreement so the EAT can deed the improved property to you.

Option #2:

Assign 100% of the ownership of the EAT to you.

Just use a formal Assignment of Membership Interest.

When you own the EAT, you receive the replacement property by extension.

Pretty simple.

Which Option to Choose?

We think Option #2 is clearly better.

Instead of setting up another closing (which takes longer and is more expensive), you can transfer the property virtually instantaneously.

Also, the same borrower can stay in place for any third-party financing.

And it’s OK with the IRS.

Now, there is one downside:

You don’t get a formal settlement statement without a formal closing.

If you are concerned about this, talk to your 1031 intermediary.

Primary Residence Conversion

A lot of investors convert their primary residence to investment property, or vice versa.

That can affect 1031 eligibility.

(In good or bad ways)

First, let’s sort out the tax consequences of conversions.

Then, we’ll help you maximize for your long-term strategy.

Sound good?

Make Sure You Know Which Assets Are More Tax-Efficient

Tax treatment for real estate depends very heavily on your use and demonstrated intend.

i.e. The government incentivizes some forms of ownership over others.

Here’s an illustrative breakdown:

So what does that mean for you?

Switching your use can deliver big tax benefits.

Before you consider converting property, you’ll need to time it so that you get the MAXIMUM benefit.

You Can Permanently Exempt Capital Gains Taxes by Converting a Replacement Property

Here’s a common scenario:

- Taxpayer sells an investment property.

- Taxpayer is nearing retirement.

- Taxpayer wants to use proceeds to buy a dream retirement home.

Of course, the taxpayer doesn’t want to pay 20-30% to the IRS.

That’s why this is such a popular topic on real estate forums.

If the taxpayer immediately trades into a new retirement home, the sale will not qualify for a 1031 exchange.

The solution?

1031 exchange into the home, but don’t occupy it.

Rent it out for a while instead.

(In this industry, this is sometimes called “seasoning” a property)

After two years, the taxpayer can move into the property and treat it like a primary residence. The IRS will not retroactively take away the tax benefits of the exchange.

And the best part?

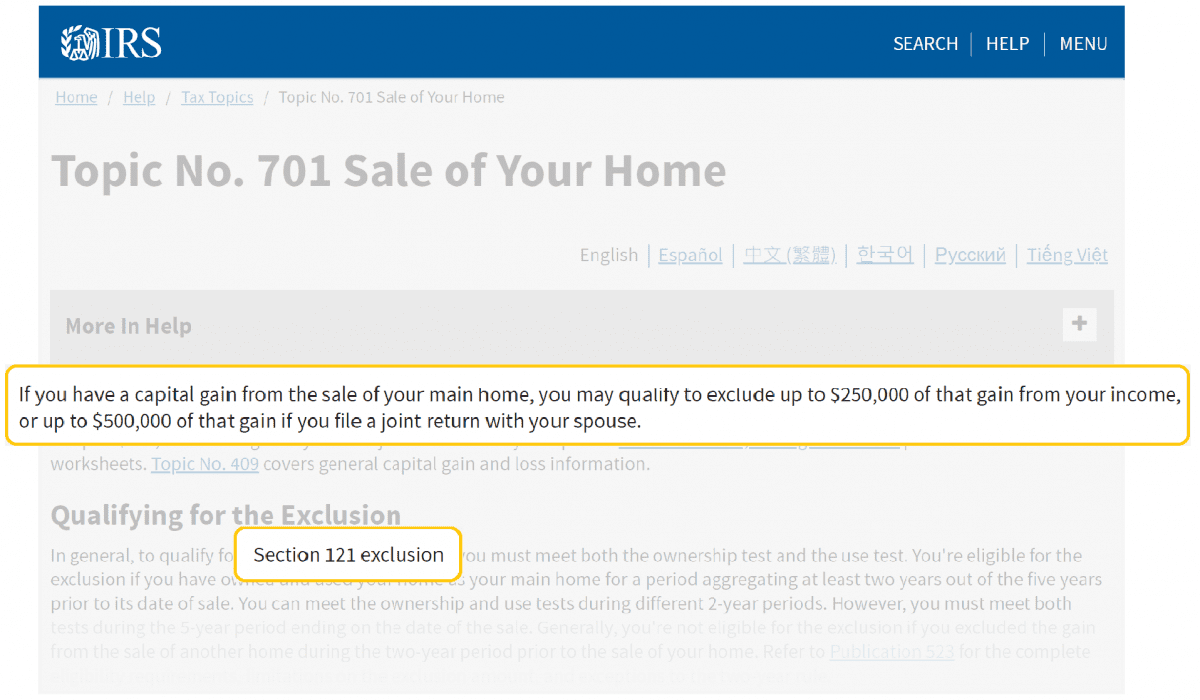

This property can later qualify for capital gains exclusion under IRC Section 121.

That means no taxes on $250,000 of capital gains for single filers and $500,000 for joint filers.

It’s one of the only ways to permanently get out of paying capital gains taxes.

Important Caveat

In the tax case Reesink v. C.I.R., the tax court upheld an exchange where someone moved into a property just eight months after the 1031. (T.C. Memo 2012-118)

Why?

The original intent was to rent for several years at least.

Then one of the owners became disabled and lost a lot of income. To cope, the owners decided to sell their principal residence and move into the replacement property because the mortgage was lower.

While tragic, this illustrates that many 1031 rules are flexible if your circumstances change.

You Can Convert an Old Primary Residence and Exchange It

It’s less common, but we do see conversions go the other way.

Consider this:

You buy a new primary home.

But, rather than sell your old one, you decide you’d rather rent it out.

IRS Revenue Ruling 57-244 establishes that taxpayers can treat their property as investment property, full stop, after “abandoning the original residential use purpose.”

What does that mean for potential 1031 exchanges?

Well, Revenue Procedure 2008-16 says that it will not challenge the exchange of such a property if:

- you own the property for at least 24 months immediately before the exchange (defined as the “qualifying use period”)

. - within the qualifying use period, in each of the two 12-month periods immediately preceding the exchange, (a) you rent the dwelling unit for at least 14 days, and (b) your personal use does not exceed 14 days or 10% of the number of days during the 12-month period that the dwelling unit is rented (whichever is greater).

(Note: These requirements are identical for the potential exchange of any vacation property or second home)

Capital Gains Tax

Depreciation Recapture Tax

Obamacare Tax (ACA or NIIT)

Refinance Options

Can you refinance your investment property before you do a 1031 exchange?

Yes, but it’s tricky.

What about refinancing after your exchange?

That’s easier.

Let’s explore.

Don’t Refinance the Relinquished Property Just to Avoid Taxes

We want to be VERY clear:

If you refinance the relinquished property, make sure you have a legitimate business or investment reason.

Otherwise, don’t do it.

Think about it. The IRS doesn’t let you pull cash out of your exchange sale without paying taxes — even if you substitute with more debt or new cash on the replacement property.

So, the IRS won’t let you “game the system” by refinancing to take out cash just before you sell.

But what if you have an independent reason for the refinance?

That’s a different story.

Make Sure You Have an “Independent Economic” Reason

There are several notable tax cases that address refinancing a relinquished property before a 1031 exchange.

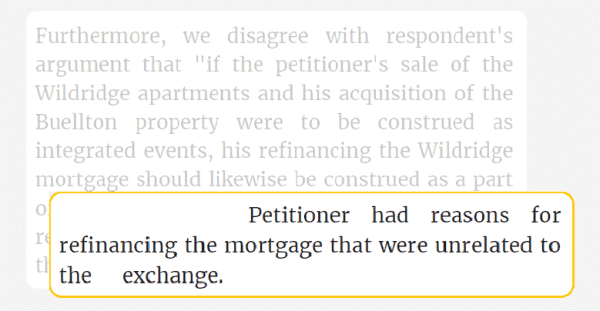

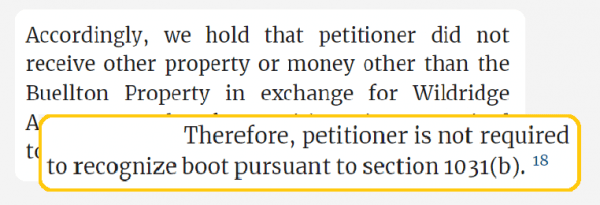

One of the most important is the 1994 case Fred L. Fredericks v. Commissioner.

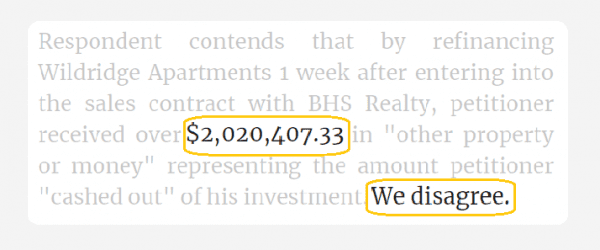

In this case, the exchanging taxpayer pulled out $2,020,407.33 in a refinance.

The IRS claimed it was taxable “boot.”

The tax court disagreed.

Why?

The taxpayer had legitimate, independent reasons to refinance.

We should also highlight that the refinance appeared to be independent of the sale itself — the court highlighted the lack of integration.

Given these facts, the court decided the refinancing exchanger did not need to recognize taxable gain.

Here are some examples of legitimate refinance reasons:

- Your business has cash flow issues

- There is an unrelated investment opportunity

- A separate rental property needs serious renovation

Here are some illegitimate reasons:

- Paying off personal debt

- Going on vacation

- Buying a personal car

Key Takeaway: Refinancing is possible, but it requires an independent economic reason for it to pass IRS muster.

Make Sure Your Lender Allows a Refinance of Replacement Property

The IRS won’t object to refinances of the replacement property.

(As far as the feds care, you can pull out cash the day after closing and use it for any purpose)

But your lender might.

In fact, it is commonplace to have 6-18 month moratoriums on refinances after a purchase.

Make sure you talk with your lender if you hope for a post-1031 refinance.

Related Party Exchanges

Who counts as a related party in a 1031 exchange?

And can you buy or sell from a related party and still defer taxes?

The answers could surprise you.

Let’s dive in.

Make Sure Your Lender Allows a Refinance of Replacement Property

Exchanges between related parties should be approached carefully.

First, though, you must know who counts as (what the IRS calls) a “related person.”

Per IRC § 267(b) and 707(b)(1), these are:

- Immediate family (siblings, spouse, children)

- Linear ancestors and descendants

- A grantor and fiduciary of the same trust

- A fiduciary and beneficiary of the same trust

- Two corporate members of the same controlled group

- An executor of an estate and its beneficiary

- Any individual, S or C corporation, IRC § 501 organization, partnership, or trust where one party owns more than 50% of the value of the other party (directly or indirectly)

Notably, the following do not count as related persons:

- cousins

- aunts / uncles

- in-laws

- step-children

Related Party Prohibitions Are Designed to Stop “Basis Shifting”

The IRS doesn’t like related-party transactions. In particular, they want to prevent basis shifting.

Let’s see why.

What is basis shifting?

“Basis shifting” is a tax-avoidance strategy wherein related persons (as defined by the IRS) exchange assets so that the person with the higher basis ultimately sells it a realizes a smaller capital gain.

How does basis shifting work?

Let’s imagine you have a property (ABC) worth $500K and it has an adjusted basis of just $150K.

And your brother has a different $500K property (XYZ), but its adjusted basis is $450K.

Properties ABC and XYZ are like-kind.

So you and your brother each do a 1031 exchange.

You trade into XYZ. He trades into ABC.

Thanks to 1031 exchange rules, your brother’s basis ($450K) carries over from his relinquished property XYZ. (Vice versa for you)

Now your brother can turn around and sell ABC without an exchange and realize a small gain of $50K.

If you had sold ABC before this swap, your basis of $150K would be used for tax purposes. The realized gain would have been $350K.

That’s a lot of tax savings!

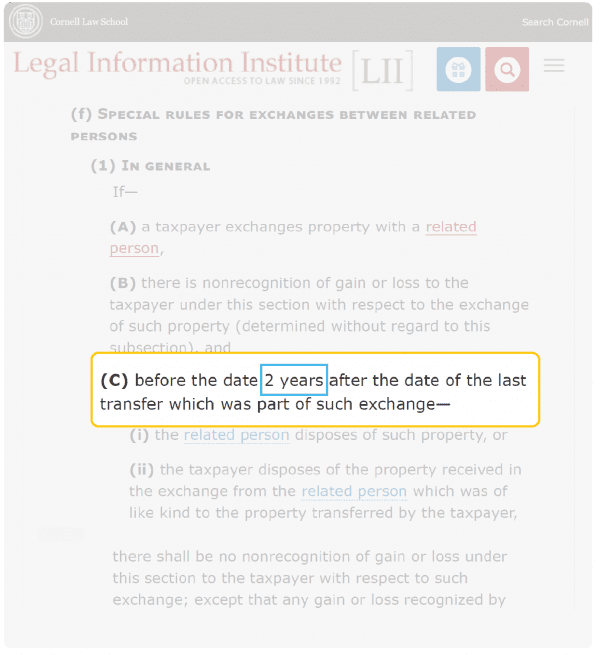

Two-year exception for direct swaps

So the IRS bans direct related party swaps with a subsequent sale.

They call this “disallowance-upon disposition”

But there is an exception.

If neither party sells their replacement property for two years, the 1031 exchange can stand.

This is from IRC Section 1031(f)(1)

Now, this is pretty uncommon stuff.

Most related party exchanges aren’t direct swaps (each receiving the other’s property)

Most are indirect swaps (only one of the related parties is doing a 1031 exchange)

We explore those next.

Easy to Sell to, yet Difficult to Buy from Related Party in a 1031

Selling to a related party is easy

As long as you plan on purchasing from an unrelated party to complete your exchange, there are no restrictions for selling to a related party.

e.g. Your father can buy your relinquished property. Or your sister.

No problem.

Important: Your spouse cannot purchase your relinquished property. All sales and exchanges between spouses are treated as gifts under IRC § 1041.

Buying from a related party is hard

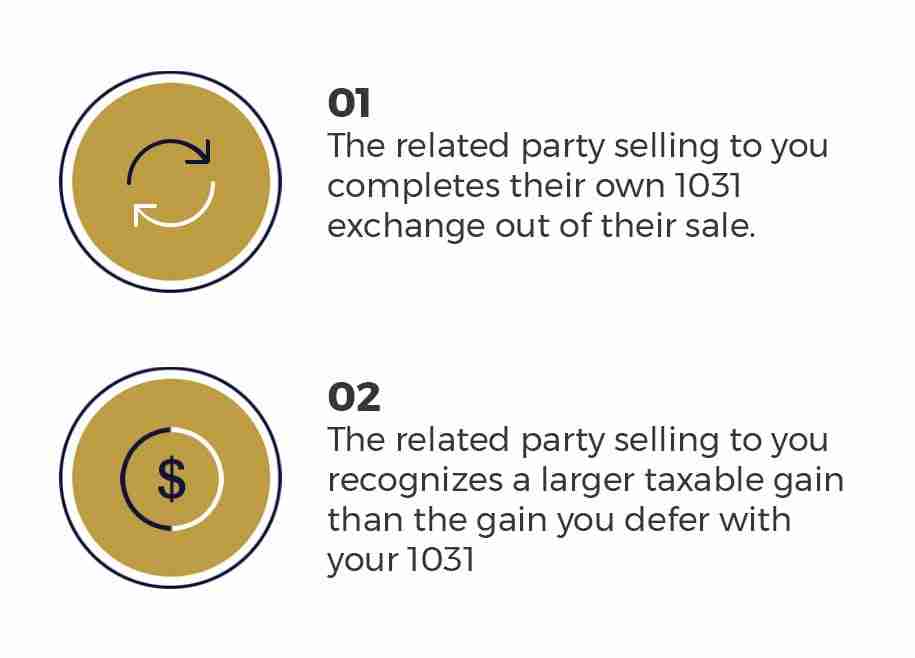

Taxpayers may NOT purchase a replacement property from anyone deemed a “related person” by the IRS.

There are two notable exceptions.

Taxpayers may NOT purchase a replacement property from anyone deemed a “related person” by the IRS.

There are two notable exceptions.

If either of these are true, then you can purchase from the related party.

Other possible exceptions include:

- Transfer takes place after you or the related party dies

- The disposition takes place because of IRC § 1033 involuntary conversions

- Related parties own fractional interests in multiple properties AND the complete exchange results in each party owning 100% of one of the involved properties

Final Thoughts

Related party exchanges are very rare. If you are interested, please call and discuss with your Qualified Intermediary. Generally speaking, it’s best to find another replacement asset.

Owner Carryback (Seller) Financing

Can owner carryback financing (installment sales under IRC § 453) and a 1031 exchange work together in the same transaction?

Short answer: Yes

Long answer: It’s REALLY tricky

Let’s dive in.

Easy to Sell to, yet Difficult to Buy from Related Party in a 1031

Owner carryback financing (“seller financing”) means any structure where the buyer is responsible for making future installment payments to the seller, just as if the seller “loaned” some or all of the purchase funds to the buyer.

It is called a “carry” or “carryback” strategy because the seller effectively carries the mortgage note after the sale, rather than a traditional lender.

How Is Seller Financing Different Inside a 1031 Exchange?

Normally, seller financing can be a really helpful tool.

For example, let’s say you want to sell a $500K property.

But the buyer can only qualify for a $300K mortgage.

(Let’s assume the buyer doesn’t have the extra $200K in cash)

So, the buyer offers to pay you $300K at closing and the other $200K plus interest — installment payments — over the next several years.

Boom.

Financing problem solved.

Sadly, it gets complicated with 1031 exchanges.

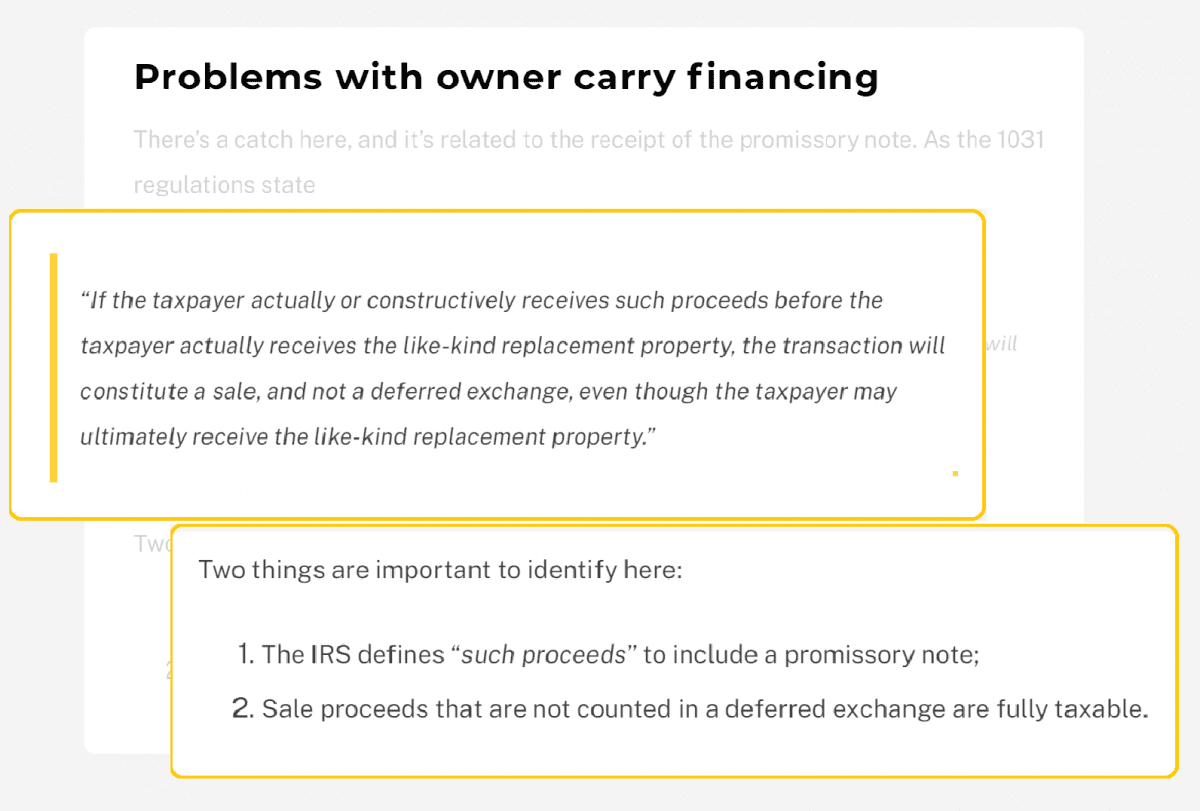

As we’ve written elsewhere, there are problems with owner carry financing in a 1031 exchange.

To put it simply:

Installment payments you receive outside of the 1031 exchange window will be fully taxable.

And…

You still have to replace the value of the note when you purchase your replacement property.

Not good.

Better Strategy #1 — Outside Cash

We recommend avoiding an owner carry loan. Instead, use a lump-sum cash loan to the buyer.

Here’s why:

- Avoids complications with installment payments under IRC § 453

. - Cash received at time of sale is immediately available for purchase of replacement property

. - Much easier to defer all taxes

Naturally, you must have the cash on hand to make the lump-sum loan (or know someone who does).

Most investors don’t have $200K lying around.

So let’s look at other options.

Better Strategy #2 — Make the Note Payable to Your Qualified Intermediary

Here’s a more interesting (and complicated) option.

When the owner carryback note is drafted, make it payable to your 1031 intermediary.

This sounds strange!

Here is the logic:

→ Any payments received by your 1031 intermediary during the exchange period now go into your 1031 escrow account.

(If you received the payments, it would constitute “constructive receipt” and be taxable under IRC § 1031(k)-1(j)(3))

→ Your intermediary can sell the note on the secondary market and put the proceeds into your 1031 account.

→ You (or a friend/relative) can purchase the note from your intermediary and put the proceeds into your 1031 account.

This single change — making the note payable to your qualified intermediary — makes a huge difference.

Suddenly you can put a lot more money into your 1031 account.

That means larger down payments.

And more value shielded from taxes.

Better Strategy #3 — Exclude the Note and Deed from Your 1031

Finally, you could exclude the carryback note and deed from your 1031 exchange.

Here’s an example.

- Contract to sell for $500K

- Buyer can only bring $300K

- You owner-carry the $200K

If you include the full value of the property in your 1031x, then your replacement assets must be worth $500K for full tax deferral.

Only you have a lot less money on hand because you’re carrying that $200K note.

Not a great spot.

So, instead you can exclude the $200K. You only 1031 exchange 60% of the property and the value of the replacement asset need only be $300K.

But be warned.

The depreciation recapture liability for the value of the owner carry note is immediately recognized.

This could leave you cash-poor and owing thousands to the IRS.

Plan accordingly.

Conclusion

We hope you enjoyed our discussion.

Now we want to hear from you.

Want advice on any other advanced 1031 strategies?

Have questions about the ones we covered already?

Or maybe you just have some constructive feedback.

Let us know.

Leave a comment. Or call / email.

That’s why we’re here!

Learn to Master 1031 Exchanges

Whether you are brand new, or need an advanced strategy, this is your go-to center for Section 1031 Exchanges.