1031 Exchange Rules and Updates (2026)

Get the basics, track the latest changes and rules, or ask our experts specific questions.

Table of Contents

What is a 1031 Exchange?

Use these rules intelligently and they can transform your investment strategy. 1031X is designed to help you do this.

Why do a 1031 Exchange?

01

Gain access to more and/or larger real estate, faster

02

Obtain greater cash flow

03

Control how and when you face taxes

04

Increase flexibility across and between asset types

What property qualifies for a 1031 exchange?

Exchange any property held for business or investment use. The taxpayer(s) that own the property must be US taxpayers, but not necessarily US citizens. The 2017 Tax Cuts and Jobs Act restricted Section 1031 to apply only to real property (i.e. tangible real estate).

Property held primarily for personal use, such as a primary residence, does not qualify for tax deferral under Section 1031.

What kind of property can you buy in a 1031 exchange?

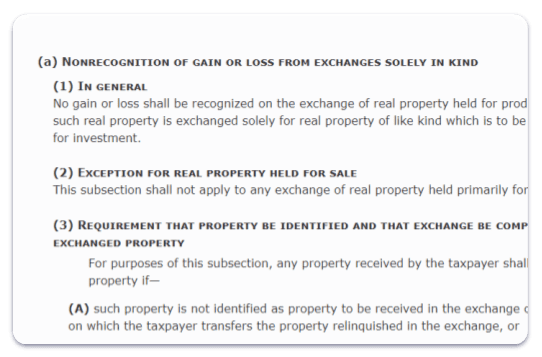

Buy “like-kind” property to what you sold ─ which is a very loose restriction. As the IRS says

Like-Kind Property

Properties are of like-kind if they’re of the same nature or character, even if they differ in grade or quality.

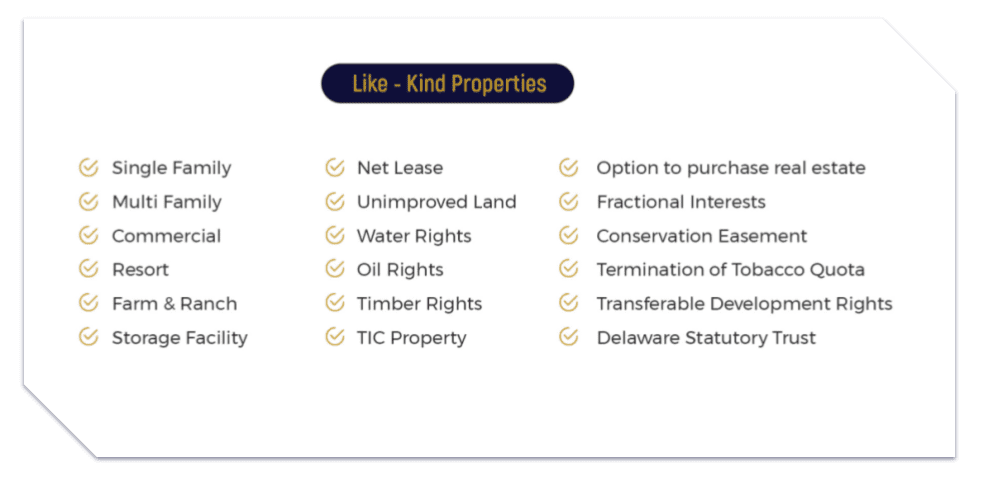

Make sure that whatever you purchase is held for productive use in a business or investment capacity. This could be land held for appreciation, residential rentals (short- or long-term), commercial space, farmland, oil and gas rights… the list goes on and on.

Use your imagination.

How does a 1031 exchange work?

To execute a successful 1031 exchange, here are the basic steps

01

Partner with a Qualified Intermediary (1031X)

02

Sell your property

At closing, the settlement agent will direct proceeds to your Qualified Intermediary. At 1031X, your proceeds will be secured in a Qualified Escrow Account at an insured deposit institution and held in your name. No funny business.

03

Identify potential replacements within 45 days

04

Purchase a replacement property of equal or greater value within 180 days

05

Report your 1031 Exchange to the IRS

When you file your next tax return, complete and attach Form 8824 to report your 1031 Exchange.

Go beyond the basics. Master your 1031 exchange.

Invest smarter.

Read practical tips and strategies.

Get instructions written in plain English, updated monthly, and designed for successful tax deferral in all 50 states.

Get simple answers, fast.

1031X makes it easy to sort through 38 exchange topics across eight major themes.

Recent Regulations

1031 like-kind exchange rules (and interpretations of those rules) change across time.

Below, you’ll find:

- IRS rules (updated for 2022)

- Treasury Regulations

- 1031 exchanges under 26 U.S.C. § 1031 (including recent and potential developments)

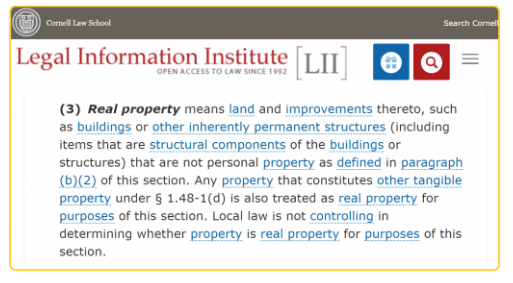

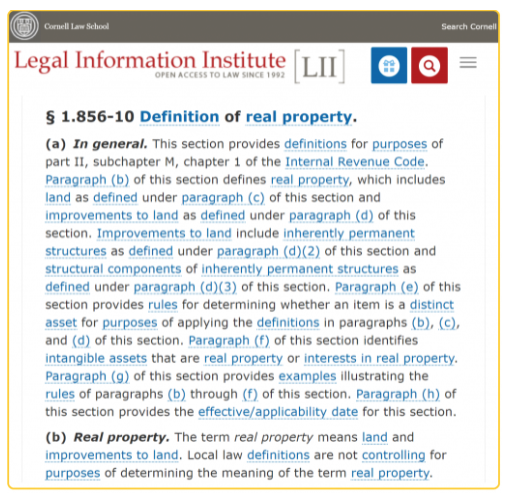

IRS Issues Final Regulations on Definition of “Real Property”

IRS Issues Final Regulations on Definition of “Real Property”

Following the publication of additional proposed regulations on June 12, 2020 (see below), The Internal Revenue Service received 21 written comments in response.

After consideration, the Treasury Department adopted the following final definition of “real property“

Source: Department of the Treasury

Read the full guidance here.

Statutory Limitations on Like-Kind Exchanges

Statutory Limitations on Like-Kind Exchanges

On June 12, 2020, The Internal Revenue Service published additional proposed regulations (and clarifications of prior regulations) addressing which assets qualify for 1031 exchanges in light of the Tax Cuts and Jobs Act.

Below, we break down the proposal into simpler language.

And we cut out a lot of the chaff.

What Is Contemplated?

Defining “real property” as it pertains to Section 1031 like-kind exchanges.

(Remember, taxpayers can only defer taxes on exchanges between “real property”)

Reason for Proposed Regulations

The Tax Cuts and Jobs Act of 2017 (TCJA) limited like-kind exchanges to “real property”. In this context, “real property” largely means “investment real estate”

Thereafter, tax-deferred exchanges for “personal property” went away (airplanes, cars, art, etc)

All of this highlighted a pre-TCJA artifact of the tax code:

There are multiple, disparate, and often incompatible definitions of “real property”

Rather than adopt one of the existing definitions, the IRS and Treasury decided to propose a new definition.

Old Understanding Before Recent Publications

Definitions of “real property” are multiple and varied across different tax code sections.

For example, the following definition is found in §1.263(a)-3(b)

New Understanding If Proposed Regulations Are Adopted

New Understanding If Proposed Regulations Are Adopted

01

“Real property” in 1031 includes

- Land

- Improvements to land

- Unsevered crops

- “Natural” land products (think minerals, trees, etc)

- Water rights

- “Air space superadjacent to land”

02

03

04

Qualified intermediaries can distribute proceeds to acquire personal property included in an exchange purchase that is incidental (i.e. typically transferred) to the real property provided that the fair market value of the incidental property is no greater than 15% of the real property.

2019-2020 Like-Kind Exchange Updates

2019-2020 Like-Kind Exchange Updates

Perhaps the most important 1031 exchange news of 2019 was the release of the IRS’ Second Round of Proposed Guidance on Opportunity Zones. This is welcome because, as those who follow “QOZ” know, the rules have been extremely vague.

These do not directly affect 1031 exchanges. That said, QOZ investments are a potential complement to (or even replacement for) 1031 strategies.

(Read more about 1031 exchanges vs. opportunity zones.)

Investors should follow proposed changes or clarifications on QOZ rules.

A few key takeaways

- Qualified Opportunity Funds (QOFs) receive more latitude to invest in raw land, to lease property, and to dispose of one QOZ asset and reinvest in another.

- The IRS defined “trade or business” in a way that likely excludes any triple-net (NNN) lease structures. This means QOFs should structure any lease arrangements to avoid NNN.

- Both a QOF and a Qualified Opportunity Zone business (QOZB) can lease property, but the lease must be entered into after December 31, 2017 to count as a QOZ Business Property.

- Safe harbors were provided to help QOZ Businesses navigate the “50% test” for business income.

- $13,150 for trusts and estates

- $441,450 for individuals

- $496,600 for married couples filing jointly

- $248,300 for married individuals filing separately

Tax Cut and Jobs Act of 2017: Impact for 1031 Exchanges

Tax Cut and Jobs Act of 2017: Impact for 1031 Exchanges

In 2017, President Trump signed the “Tax Cuts and Jobs Act” into law.

This slashed individual and corporate tax rates, increased deductions and credits, and attempted to crack down on loopholes and exemptions available to certain taxpayers — including investors attempting a like-kind 1031 exchange.

We can say “attempted” thanks to concerted efforts by major real estate lobbying groups (NAR and FEA among them) that managed to save the most important aspects of 1031 exchange regulations.

We did see some changes, as broken down below:

Repeal of all personal property exchanges

Prior to 2018, investors could exchange assets considered “personal property” by the IRS.

Examples included airplanes, collectables, works of art, livestock, franchise licenses, and classic cars. The new law only allows for “real property held for productive use or investment” to qualify for deferred exchange. In short, only real estate still qualifies.

Introduction of Qualified Opportunity Funds

The new tax law created incentives for investors to reinvest their proceeds into Opportunity Zones (OZ). Ideally, these OZs would bring economic development to historically struggling communities. Investors might be able to defer and, if certain conditions are met, exclude their capital gains taxes. Little guidance was given on OZs and their functionality.

While they do not interact with 1031 exchanges, some OZs can function as an alternative.

(Update: New regulations and revenue rulings issued on October 19, 2018 clarified many OZ details.)

Increase in bonus depreciation

Also modified were the allowable depreciation rules under IRC § 168(k). Under the new law, businesses could immediately deduct the full cost (100%) of many kinds of personal property; this amount drops by 20% per year after 2022 until it reaches 0% in 2027. This eases the loss of the personal property exchanges.

Change in alternative property depreciation system

The standard property depreciation limits (27.5 years for residential; 39 years for nonresidential) remain unchanged. However, the alternative depreciation system for residential property changed from 40 years to 30 years.

Note: While much of the new tax reforms went into effect in 2018, some rules, such as the repeal of the individual mandate under the Affordable Care Act, did not become active until 2019.

Taxpayer Relief Act of 2012: Impact for 1031 Exchanges

Taxpayer Relief Act of 2012: Impact for 1031 Exchanges

Change in Capital Gains

Change in Capital Gains

- The rate for long-term capital gains (and dividends) will remain at 15% for individual taxpayers with incomes of $400,000 or less ($450,000 for married taxpayers).

- The rate for capital gains (and dividends) exceeding this level of income will rise to 20%.

The new Medicare tax of 3.8%

The new Medicare tax of 3.8%

In addition, as of 2013, the IRS imposes a Medicare tax of 3.8% on income (including capital gains from the sale of investment real estate) for” higher-income” taxpayers.

The income threshold for this tax are lower than the increased rates on capital gains explained above. Taxpayers with gross income of $200,000 ($250,000 for married taxpayers) will pay the new Medicare tax. This tax will only apply to the amount of gain which causes adjusted gross income to exceed this high-income threshold.

Moreover, two exceptions exist to this new tax:

Real estate owned and used in a trade or business (as opposed to held for investment), and

Real estate sold by real estate professionals. A real estate professional is a taxpayer who spends more than half of their year (and at least 750 hours) in real property businesses in which he or she materially participates.

Remember, a successful 1031 exchange also defers any Medicare tax. Taxpayers frequently underestimate the amount of tax they will be liable for when deciding not to 1031 exchange. Don’t forget to take into consideration the recaptured depreciation, state and local taxes, and now these new additional taxes.

Capital Gains Explained

Capital Gains Explained

1031 (or “like-kind”) tax exchanges allow taxpayers to defer payment on taxes when they sell investment or business property. The taxpayer must then reinvest into another investment or business property of equal or greater value.

Broadly speaking, investors owe two types of capital gains taxes after selling investment property.

Long-Term Capital Gain – Increase in value from the original purchase price.

Depreciation Recapture – Recapture of depreciation expenses taken by the investor since acquiring the property.

Here is a little background:

Capital gains taxes were decoupled from ordinary tax rates following The Revenue Act of 1921. Suddenly, a window opened for treating gains made on investments differently than traditional income sources.

Section 202(c) of The Revenue Act of 1921 also created the first predecessors to modern 1031 exchanges, which allowed both like-kind and non-like-kind exchanges via a deferral strategy.

So began a nearly 100-year dance between investors and lawmakers about the necessity and merit of tax-deferred reinvestment.

Learn to Master 1031 Exchanges

Whether you are brand new, or need an advanced strategy, this is your go-to center for Section 1031 Exchanges.